Who really has overcapacity in auto industry?

Who really has overcapacity in auto industry?

In the past few months, I’ve probably heard enough repetition of Chinese “overcapacity” to pull my hairs out. The stats thrown around was 40 million in capacity, but only about 22 million being sold every year.

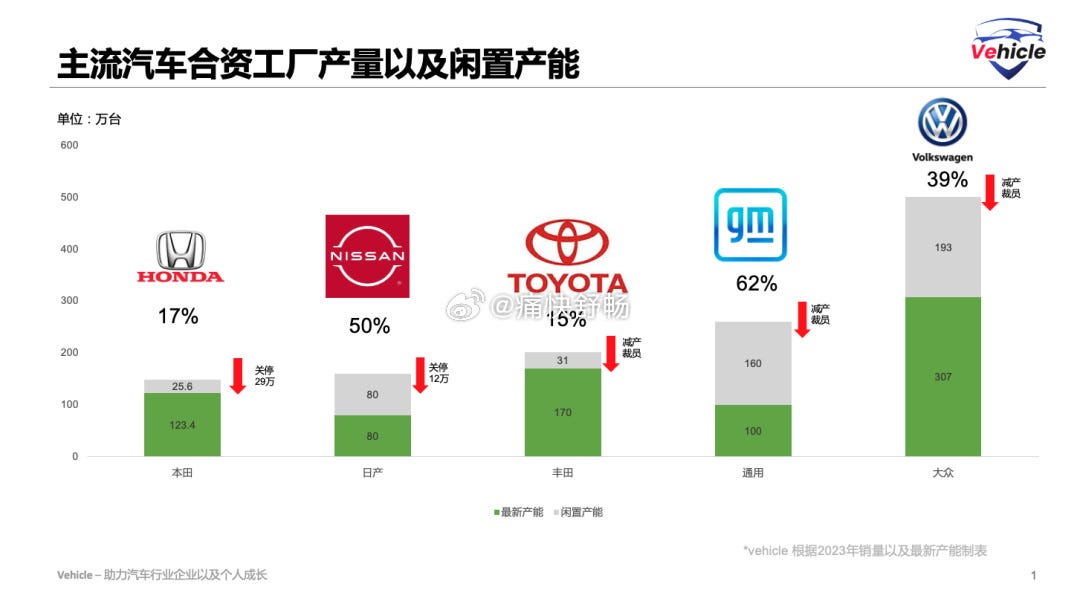

The entire idea of overcapacity is silly to me at a time when we are rapidly transitioning from ICE to NEVs in China. As such, there will obviously be excessive amount of ICE capacity in China. While, some Western analysts were willing to acknowledge that the overcapacity exists in ICE, they failed to acknowledge that all of the overcapacity is by legacy JVs. The picture below shows some numbers from 2023.

As you can see, GM has 2.6 million capacity, but only sold 1 million cars in China last year. VW has 5 million capacity, but only sold 3 million cars last year. Only Toyota and Honda have relatively high utilization on their plants. It seems like they are also proactively cutting back on unproductive factories.

Recently, I reported on the August sales according to CPCA. VW sold 170k units, Toyota sold 135k, Honda 57k and GM was no where to be found in top 10. Based on SAIC’s own report, GM sales was down 82% YoY in Aug to just 16k. Even including less bad numbers from earlier part of the year, GM is down 59% so far this year and has sold just 256k vehicles. At this pace, GM will have a hard time even reaching 350k sales for the full year. And at this current pace, GM will be using just 200k out of 2.6 million capacity. Honda is on a 600k per year pace out of 1.5 million capacity. Volkswagen is currently on 2 million sales per year pace out of 5 million capacity. Clearly, overcapacity is all around.

I don’t blame foreign automakers for hesitancy is closing old factories. China was the major profit center for VW and GM for many years. The NEV transition has happened so fast, that their CEOs simply have not fully come around to the new reality. This level of denial-ism is common amongst us.

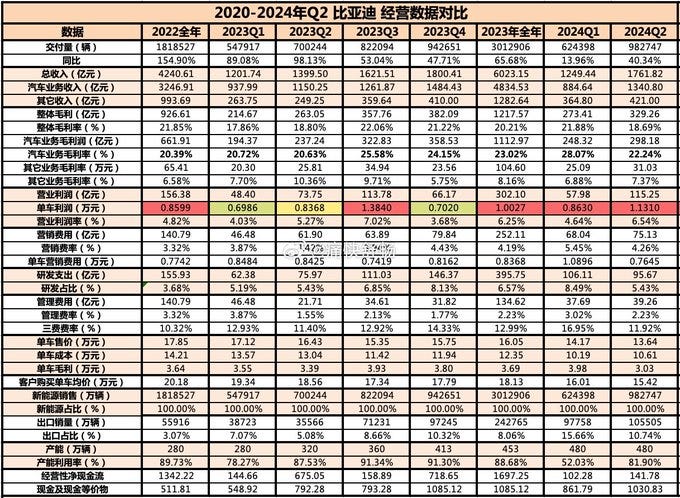

And then we can switch to looking at BYD. We know that BYD was extremely capacity constrained back in 2022. By 2023, this was no longer the case. But in the past month, backlog has started building up again as order book is growing much faster than production rate. For two months now, its reports sales is higher than its production. Its domestic registration + export have been much higher than sales. That means, it has been significantly de-stocking recently due to slowness in ramping up production. Even when it was not facing this level of demand, BYD was still reaching utilization of 80% back in Q2.

See above for capacity (4th from bottom in 10k) and utilization (3rd from bottom). It’s capacity in Q2 was 4.8 million with utilization of 81.9%. Utilization was in the 90+% range back in second half of 2023. Clearly, BYD operates close to full utilization in order to minimize its cost.

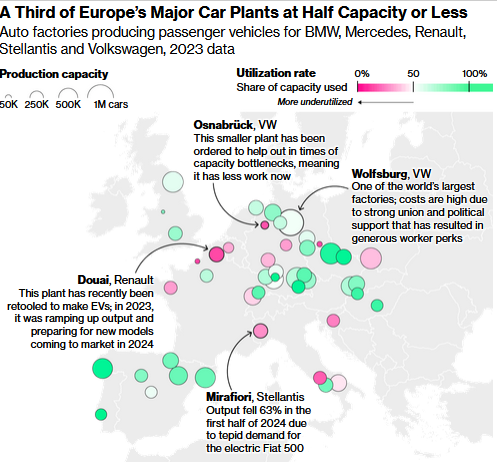

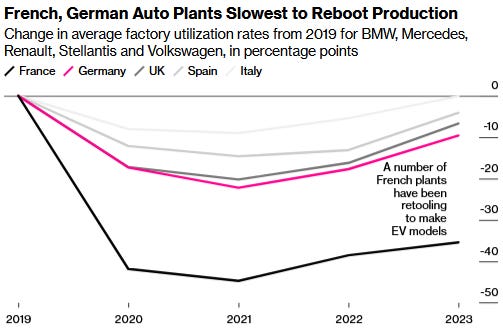

Which brings us to the Germans. Recently, Volkswagen reported that it is considering to close plants in Germany. As reported here, VW sold 9 million cars last year out of 14 million capacity. As I mentioned above, it’s currently on pace for a lot lower in China in the second half of the year. Since European auto sales are down YoY, VW has a lot of “overcapacity”. Beyond that, China was historically a profit center for VW. That means, profit in China can offset weaknesses and lower margin in other regions like Europe. As profit in China plunges below global average, VW can no longer afford to keep some of its European plants open. The level of overcapacity for VW and other European automakers can be seen in this Bloomberg article.

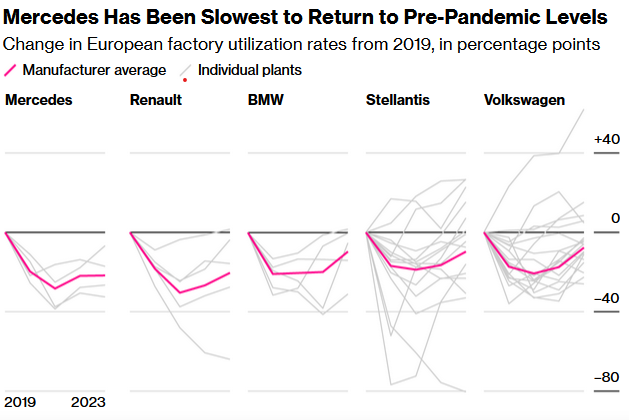

The Europeans somehow have the nerve to say China have overcapacity when a third of its plants are operating at below 50% utilization. It’s easy to see why when considering how low utilization has been vs 2019.

Tough times ahead for all the European automakers. The pain for Europe doesn’t stop just at VW or Germans. The French plants are far and away the most underutilized.

It takes a lot of capex to transition from ICE to NEV. Tier 1 suppliers aren’t always the same when batteries, chips and smart car tech are majority of the cost on an EV. Traditional suppliers like Bosch, Continental, ZF and Valeo are cutting a lot of people, because declining ICE production is taking a huge bite out of their revenue stream. Legacy companies typically have very high fixed costs. They cannot get margins higher unless they are willing to make huge layoffs and close factories. While much of the focus have been on EV price war in China, the price war between Tier 1 suppliers is just as fierce. Bosch China has been public in stating how damaging it is to their bottom line. However, this is not a battle they are giving up. Once you leave China, you are never coming back in.

The economics of ICE production will continue to worsen as utilization comes down and tier 1 suppliers go into financial difficulties. Even so, legacy European automakers are still making money on ICE and losing money on EVs. As such, they are continuing to lobby regulators to cut back on EV transition deadlines and CO2 emissions target. None of the EU automakers are doing what’s necessary to actually transition to EV production, because it would cause stock prices to tank even more.

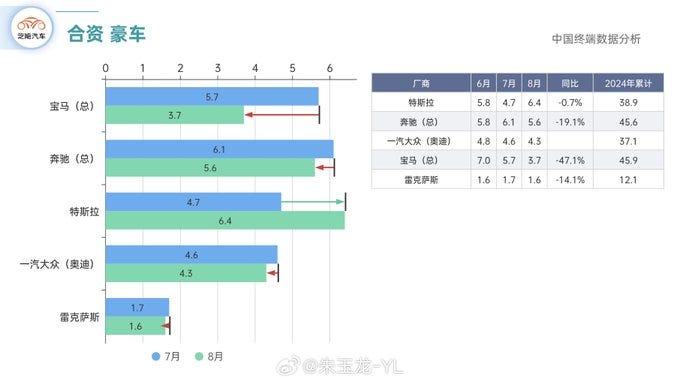

As such, the problems of slow EV transition isn’t just affecting mass market brands. It is also severely affecting the German luxury brands. As seen below, huge sales declines in August from BMW, Audi and Mercedes.

BMW sales is down 47% YoY. Mercedes is down 19%. One of the few notable outcomes of EU EV tariffs (And Chinese retaliations) is Mercedes deciding to produce GLE in China. All of this shortfalls in China sales and production shift will cause further decline in their Chinese factory utilization as well as European factory utilization in the case of Mercedes. As recently as 2021, China accounted for nearly 40% of BMW sales globally. As recently as 2022, China accounted for 37% of Mercedes sales globally. Can BMW afford a massive 20% sales drop globally (caused by losing 50% in China YoY)? Can Mercedes afford a 10% sales drop globally (caused by 20% drop in China YoY)?

The story of global auto sector overcapacity is also the story of legacy automakers seeing ICE demand crash overnight and unable to move to EVs. There is simply no evidence of EV overcapacity in China at the moment. The price war in China is caused by too much competition rather than too much capacity. That’s a situation only time and market will fix.

Great piece, the Western car makers simply missed the boat on EVs through their own bad decisions / short term profit maximization. As you say, the loss of the Chinese sales remove a financial buttress for their domestic operations with the result that they will have to close domestic low-utilization and loss-making plants and will find it very hard to fund the ICE to EV transition. All the while as the Chinese EV manufacturing leaders get better and better, and build more and more plants in Europe.

A major issue holding back exports by the likes of BYD is that they have to increase capacity so fast just to maintain domestic market in a market growing at 40% a year. Australia and the UK, which have not erected anti-China tariff walls, may be a leading indicator of what happens to the EU once the Chinese plants are up and running and the Chinese market becomes saturated (by end of 2026 at the latest most likely).

Yes it has been really bad argumentation about Chinese "overcapacity" and exports. Good to see Bloomberg talking about European overcapacity and that you write about the suppliers. Still I wonder if getting outcompeted and overcapacity in China is only a JV problem?

It seems fierce competition is hurting some of the domestic brands too. In the overall domestic sales this year one of the largest Chinese brands Changan lost 22%, BEV brand Aion lost 29% and Haval is down 32%. In BEV brands domestic sales we also see Neta losing 43%. This I would guess must create overcapacity if they don't directly close plants or let another brand use them. Changan and Haval are growing exports this year, so that would mean capacity going from domestic to export, sure this is ICE not EVs as often claimed. While looking on exports MG falling 21% this year could mean overcapacity, without exports.

While some foreign brands are losing on total sales they are starting to grow in domestic BEV market this year like VW up 51% and Toyota 44%, even BMW up 15%. So they are behind but some slow transitions are going on.

It would be really interesting to get a nuanced picture of the domestic market and exports. Any good explanation for Aion, Neta and MG losses in sales? Then another deeper discussion is who is selling with a profit in the market, as NIO, Xpeng, Xiaomi and so on is growing capacity while losing capital. These companies have so far probably only made money for suppliers as CATL and BYD.

Changan falling and failing transition (slower BEV growth than VW, Toyota and BMW) should be discussed looking also on their "new JV" brands Deepal and Avatr. I remember some years ago when BAIC was leading the EV charts and then completely falling away. There could be some relevant back stories to these newer losers too.

Personally I will stick on my substack to write about BYD with some glances on the main competitors, but it would be great to read an indepth piece on the domestic competition!