Why is hydrogen important?

Those who follow me will notice that I’m a huge proponent of hydrogen in energy transition. I’m a real believer. Recently, I saw this photo of “Hydrogen Ladder” and wanted to just put my thoughts on this. In many ways, if crystallizes my own view on where green hydrogen, ammonia and methanol will be deployed. This is a very important industry, since just A and B in the ladder requires 6x all existing wind & solar. It’s possible that the actual demand could be higher than that depending on various factors. But given China’s unique role as world’s renewable industry factory, increasing demand for its solar, wind, battery and grid related products is a huge boon for its industries.

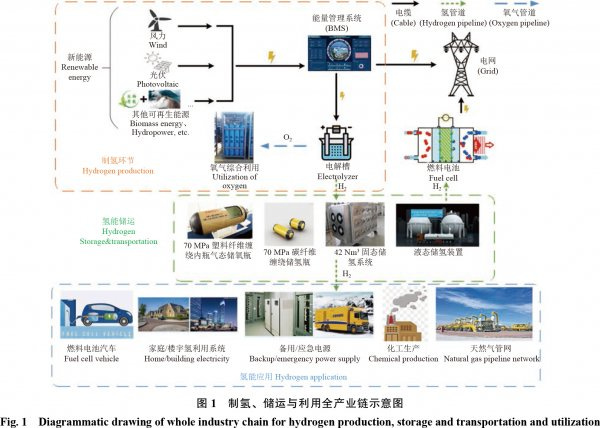

In the past few months, “overcapacity” has become the key theme among Western politicians looking to fight back against China’s dominance in energy transition sectors. China’s dominance in solar industry has fueled a huge growth in renewable energy generation leading to lower carbon footprints in recent months. However, there is a limit to how much China’s electric grid can add in terms of solar and wind capacity due to grid needing more ESS capacity, smart grid tech, long range UHF lines and installation capacity (workers and machines). Most of China’s abundant renewable resources are in the north and west, while the energy consumers are in south and east. How does hydrogen solve this problem then? We know from the following chart that you can have renewable energy generation stores in battery management system, which can power electrolyzer to generate Hydrogen and store additional power in battery to be used later when it’s not sunny outside or when wind is not blowing. All of this requires significant amount of wind turbines, Photovoltaics, battery, chips, electrolysis and hydrogen containers to work. China has already built a fully domestic supply chain for all of this. And that supply chain is continually adding more capacity as demand increases.

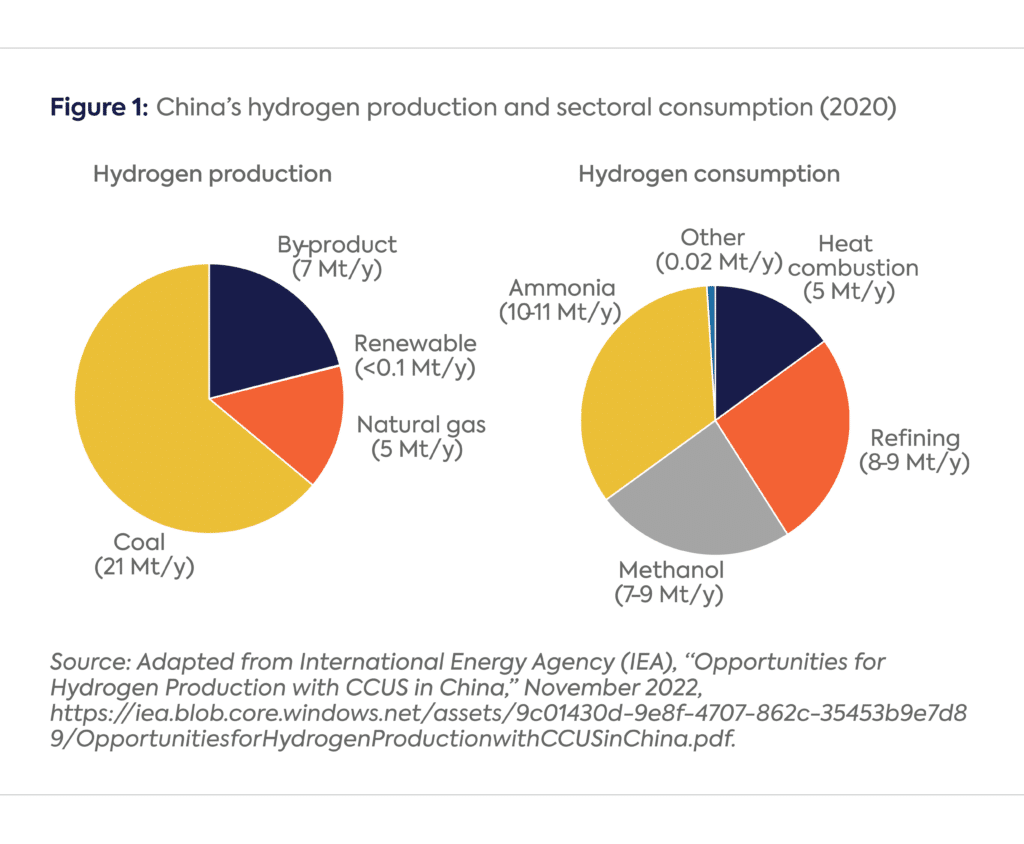

But where is all this production going to? Well, the first part is getting the cost down for applications that requires hydrogen. China is the world’s largest producer of Hydrogen (mostly through coal). It produced 37.8 million ton of Hydrogen in 2022 (102 million ton were produced worldwide). A lot of this were used in methanol and ammonia production. A lot of this were used for industrial purposes and refineries. A very small portion is also used for transportation. This is from 2020:

Looking back at the hydrogen ladder, fertiliser, methanol, steel, shipping, chemical feedstock, jet aviation and long duration grid balancing are listed as some of the most unavoidable use cases for hydrogen. We are now already seeing green hydrogen related projects getting under way in China.

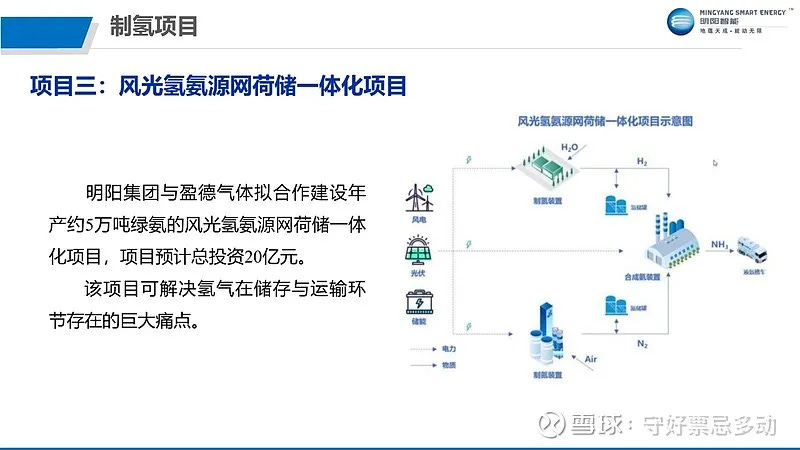

Most recently, a new 500k ton per year green ammonia project (produced through 101.3k ton per year of hydrogen) kicked off with the goal of combining with captured CO2 from Coal usage to produce 880k ton of green Urea which is used for fertilizers. If we consider all of the farming globally that will need green fertilizers in the future, this is a huge market. Getting to that point will require huge ramp up in wind, solar, ESS, electrolysis, ammonia synthesis, CO2 capture, liquid CO2 generation, CO2 transports, ammonia transports and equipment that combine CO2 with ammonia to generate Urea. You can see from Mingyang’s slide below on how ammonia can be generated.

Another really big usage case is methanol to be used in various chemical sectors. There are a long list of projects. As of January of this year, a total of 4.78 million ton of green methanol have already been announced for various purposes. This figure has only grown since that point.

Sustainable Aviation Fuel is another large future market for Green Hydrogen. Diagram below shows the process with which we can create SAF from H2 and Biomass along with captured CO2

Recently, CEEC just signed a deal to build a new 600k ton green methanol and 100k ton green aviation fuel with government of TongLiao, in Inner Mongolia. This is just one of many projects producing green aviation fuel that have popped up around China. The market for this type of fuel is very high among airlines looking to achieve ESG targets. I anticipate that major airports in China will soon start of advertise that they have SAF available for any airlines and it will be a very in demand service.

Shipping fuel is another application of Green Hydrogen. Back in November, Maersk signed a landmark agreement with Goldwind to purchase 500k ton of green methanol of shipping fuel per year. Goldwind has since commenced project and is supply wind turbine as well as other equipment needed to eventually produce 500k ton of green methanol a year. It doesn’t stop there. COSCO shipping has recently signed deal with CGN and ChimBusco to produce 200k ton of green methanol per year through 500MW of wind turbine park that CGN is building. Works for green shipping fuel does not stop here. Numerous ports around China are building methanol refueling centers to support all the methanol fuel (and also dual fuel) ships that are coming online. In December, Mingyang signed deal with Hainan province to produce 3 million ton of green fuel. Part of that deal entails Hainan building refueling center for global shipping. It didn’t stop there, Shanghai finished its own green methanol refueling center in Yangshan port in March. 280k M3 of methanol storage has been made available here. In May, Mingyang also signed deal with Shenzhen government to also develop their methanol refueling center. The most interesting project I have seen is the one by the Northeastern provinces to supply green shipping fuel in April. They have the goal of producing 32 million ton of green shipping fuel by 2030! They would like to ship 29 million ton of green methanol just from Liaoning province by 2030.

I think that’s the key here. So much solar, wind, electrolysis and battery capacity won’t connect to grid right away. However, China can use that to produce green energy in terms of shipping fuel, aviation fuel or methanol/ammonia for various chemical applications that can be sold abroad. Western countries always complain about China dominating green energy supply chain. Okay, then don’t buy the machines that produce green energy. China can use its own machines to generate green energy and ship that to you. That’s the key here. Green methanol and ammonia allows easier transportation of green energy. Eventually, that will allow China to become a net energy exporter rather than world’s largest energy and hydrocarbon importer. That’s a huge change for everyone.

It’s important to grasp that hydrogen is finally above all a way to store nuclear energy. Full stop. Abundant nuclear causes, indeed requires, abundant hydrogen.

Happily, the drowsy USA energy system seems to stir with the switching on of the two new Vogtle nuclear plants in Georgia. Tom Fanning, recently retired CEO of Southern Company to whom we are most indebted for the plants, was the rare CEO who did not succumb in the land of the Lotus Eaters. On 31 May in Georgia, the US Secretary of Energy rightly said, “Okay, two down, 198 to go,” by 2050. Let’s make a growing fraction of the 198 reactors high-temperature machines that can thermochemically make the hydrogen that sustain the USA on the track of Decarbonization on beyond methane.

https://rogerpielkejr.substack.com/p/the-environmental-trinity?utm_source=post-email-title&publication_id=119454&post_id=145916873&utm_campaign=email-post-title&isFreemail=true&r=16k&triedRedirect=true&utm_medium=email

Between 50 and 80 percent of the energy value of clean electricity is lost in the process of making hydrogen and then burning it to generate electricity.

Meanwhile, enhanced CO2 is greening the planet. The supply of CO2 that is available to plants via the atmosphere is likely the most limiting circumstance faced by plants. Increased CO2 enhances plant water use efficiency. So, grain yields are increasing due to this, fertilization, improved weed control and better soil management. The deserts are greening.