Future of SiC industry in China

I was drawn to write this piece as my first substack piece after lengthy look at China’s EV supply chain. Of which, SiC is a crtical part of automaker plans to increase efficiency of their electric drivetrain and on-board charger.

There have been many industries where Chinese companies are the OEM (Original Equipment Manufacturers) that heavily relied on Western suppliers when they started off. Eventually, they were able to either find local suppliers or make it themselves. There are other cases where Western OEMs entered Chinese market with commanding market share only to watch it dwindle away as domestic companies became more and more competitive.

One prime example is when Chinese oil/chemical companies started to build up refineries for more advanced petrochemical only to be dismissed by Western incumbents. Over time, the Chinese companies did take over local market share as the new refineries came online and many Western companies lost their share.

I bring this up after reading Doug O'Laughlin's piece on SIC as well as Digitimes Article that more than half of World’s Silicon wafers might come from China. Both pieces are on the right path in noting that China has a lot of SiC wafer capacity coming online. And Doug correctly noted the disastrous consequence on Wolfspeed which sold its GaN RF business and bet the farm of SiC. I have not studied the other business plans of Wolfspeed, but if all they have is SiC, investors should flee with their money.

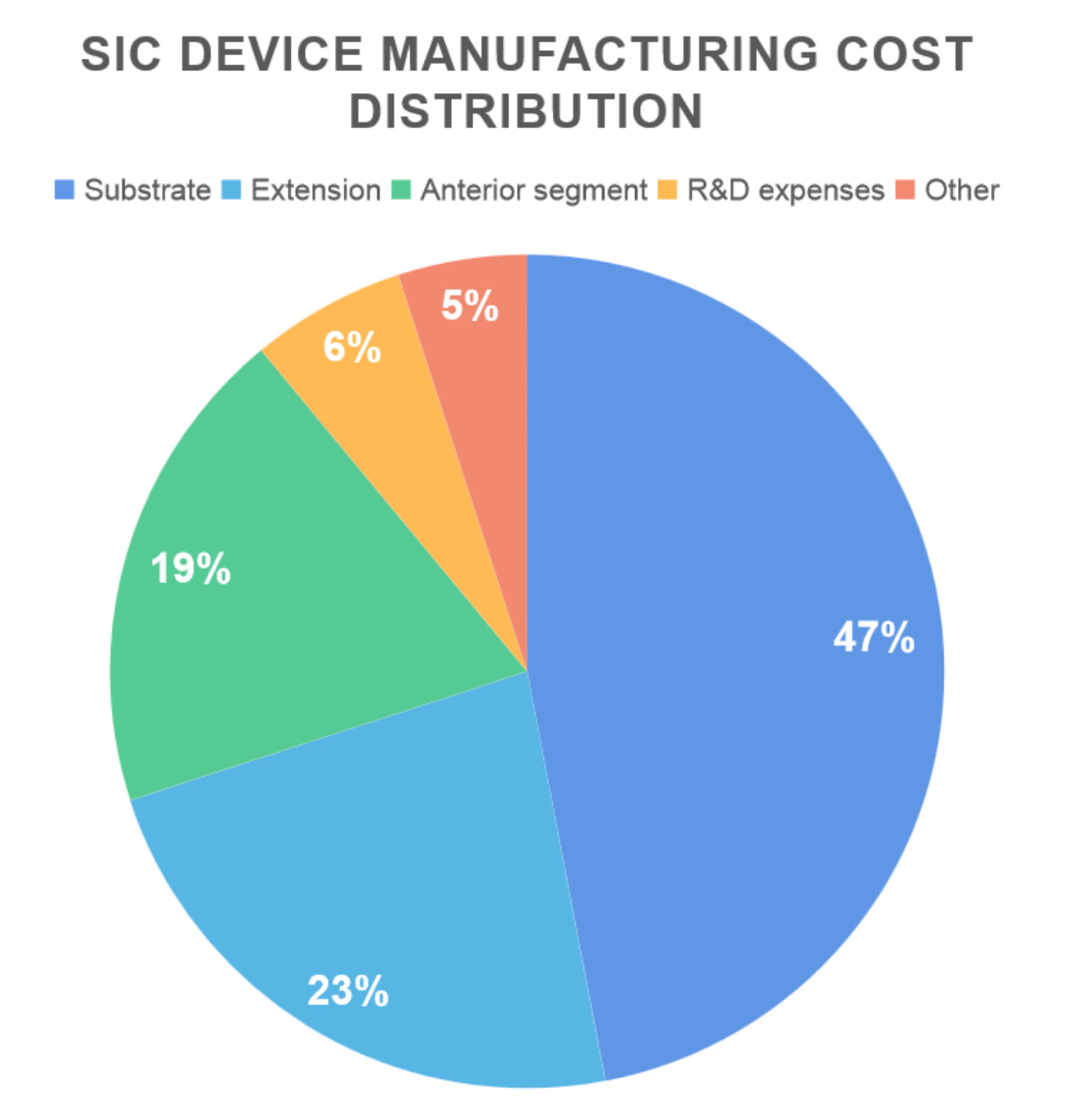

This is normally what I see the breakdown of SiC production cost. You can see that Substrate is 47% & Epitaxy is 23% (so wafer production itself is 70% of cost)

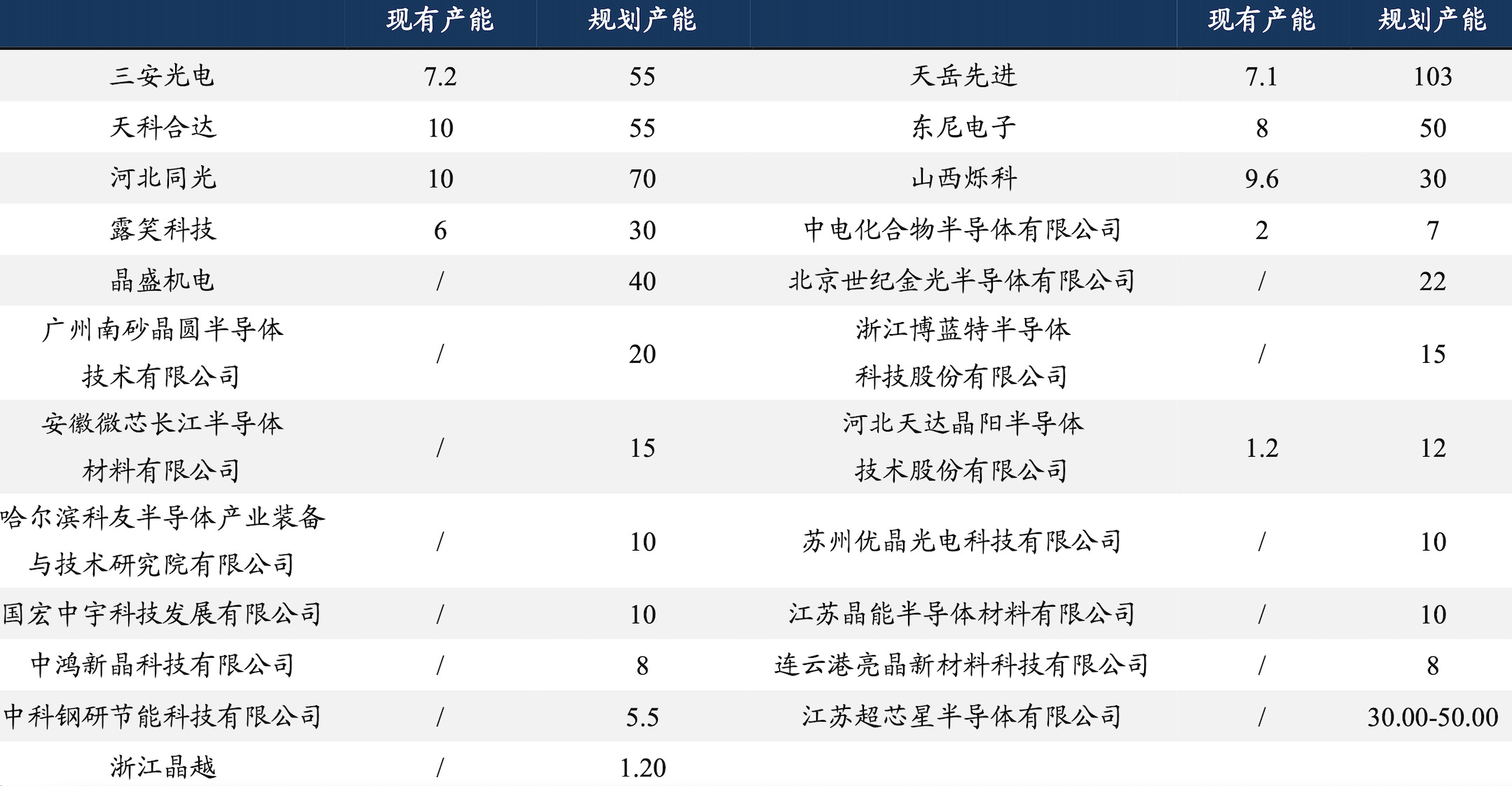

Substrate is also where Chinese firms have really been building capacity as seen below where you see the 2022 capacity vs 2026 project capacity. This chart is compiled by a Chinese research firm and does not contain all the projects. I definitely know quite a few more. Even this table shows 10x in capacity expansion

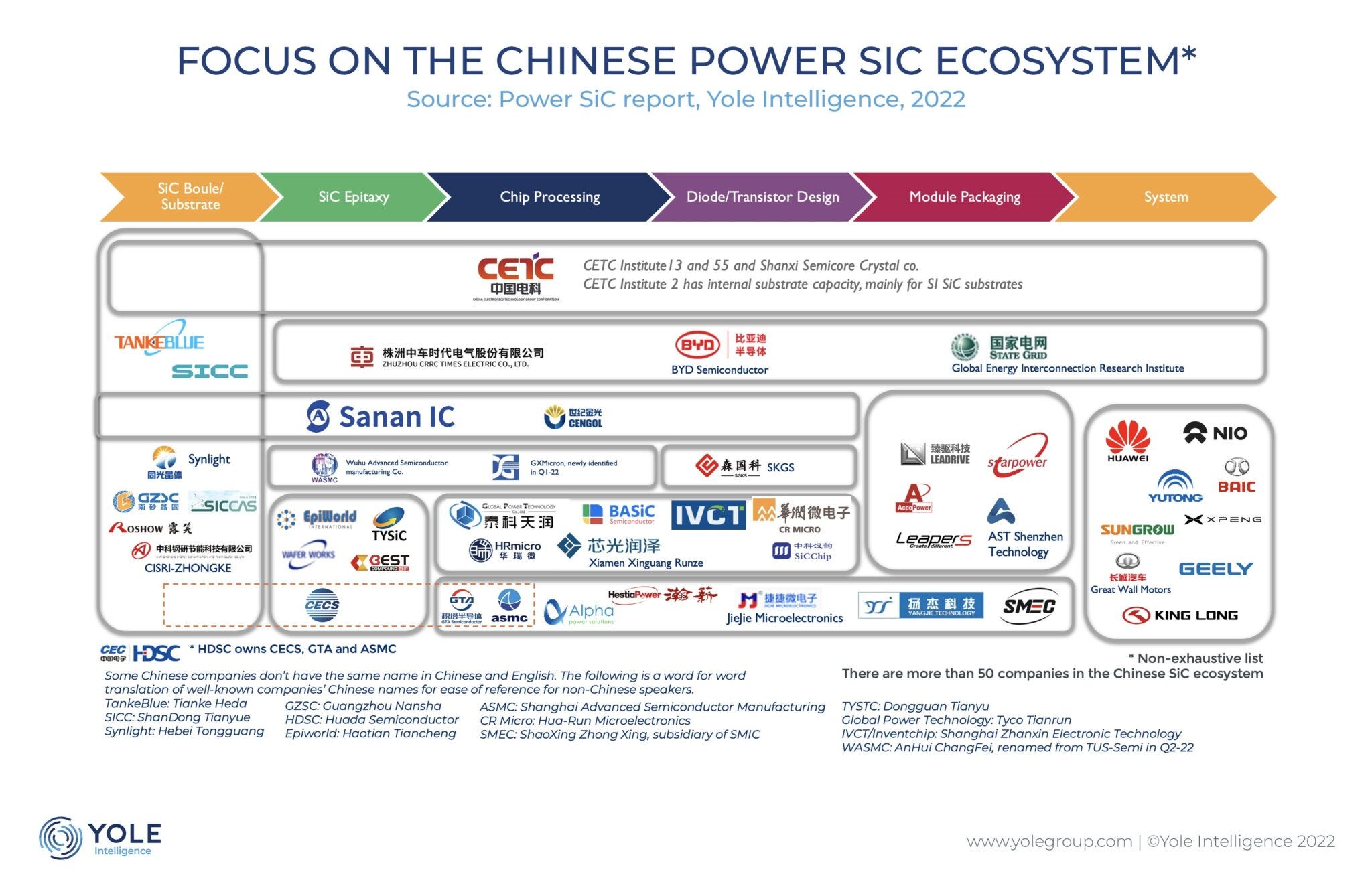

We know Sanan is supplying substrate for its JV with ST Micro. We also know SICC/TankeBlue are supply substrate for Infineon’s products to Chinese customers. So it is likely almost all SiC sold in China by 2026 will be using Chinese substrate. Clearly, China is the largest SiC market in the world due to demand for new energy cars, trucks, buses, PVs, smart grids, electric train/traction, ESS & other industries where energy efficiency really matters. And China is pretty dominating in all these fields with mostly complete supply chains.

So, you may ask, doesn’t Western companies dominant SiC? Well, China does have a full SiC supply chain as you can see below

And this goes beyond each step of production all the way to the equipments that make them. This is not an industry where China is concerned about sanctions at all.

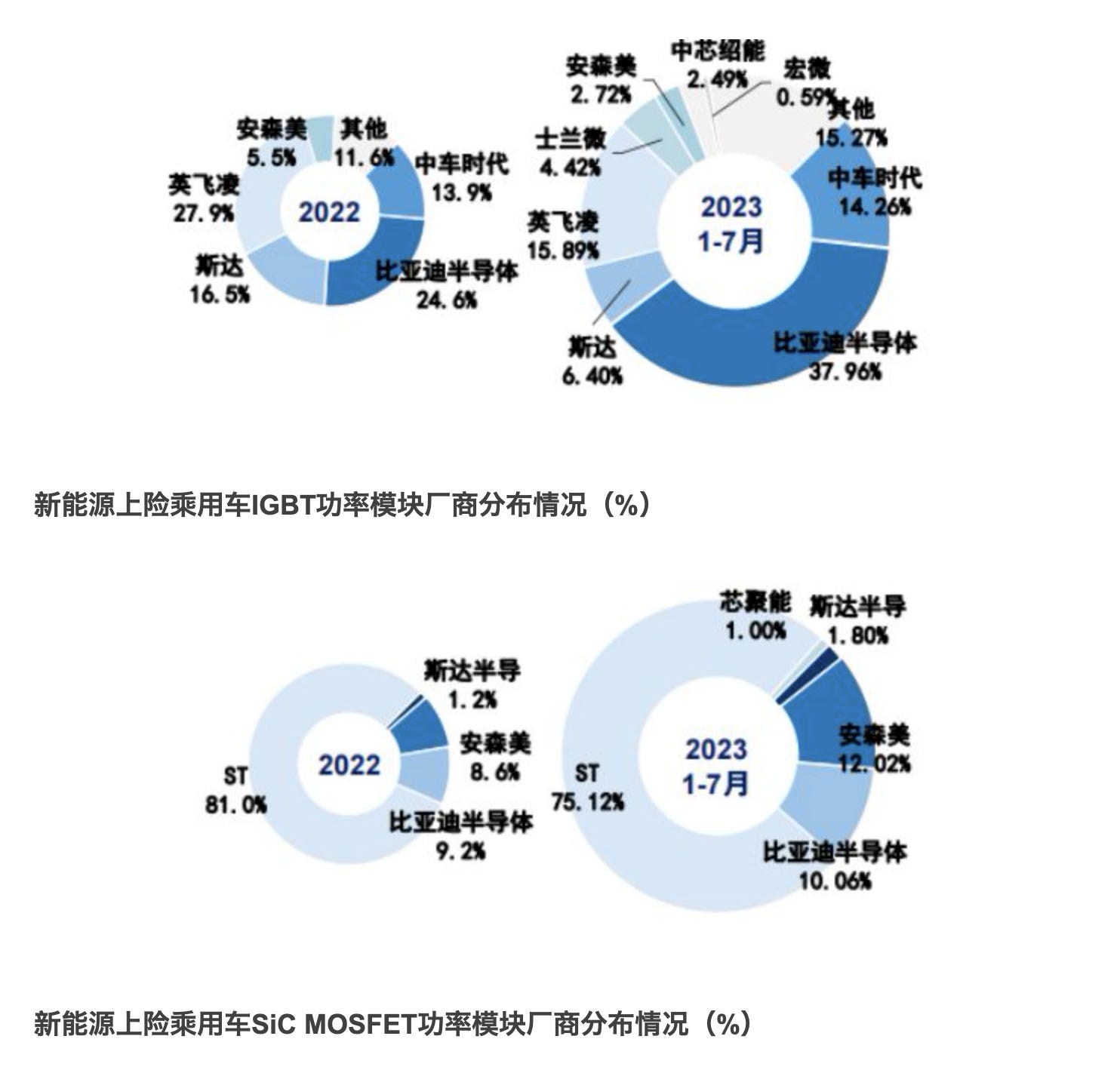

Here is the current market share situation in China’s EV market. Top image is IGBT module share in 2022 & 2023. BYD Semi leads here at 38% in 2023 up from 25% in 2022. Infineon down from 28% to 16%. As BYD increased production & new players like Silan/SMEC/CR Micro came in, Western chipmakers are getting wiped out

Section below is Sic market. Thus far, ST+Onsemi has held steady at close to 90% due to the overwhelming demand from Tesla & Nio. However, that is expected to change going forward. A whole bunch of EVs on 800V platform heavily using SiC has entered market in past few months. Tesla said it will reduce SiC usage in its cars. At the same time, BYD Semi is making huge expansion from its current 10% market share. BYD is investing in substrate, epitaxy, chip design, fabrication & packaging. In 2022, it outlined plan to increase production to 20k wpm in 5 yrs (vs 1.5k wpm now). Aside from BYD, ST Micro has partnered up with Sanan. Many other domestic Sic makers have entered the market this year. Their products are likely to finish validating soon & be used on EVs next year. For example, SMEC has shortly increased capacity from 2k wpm in June to 4k wpm in Sep. Silan is increasing capacity from 3k in June to 6k by end of year. SMEC is now the largest IGBT supplier in China. They have huge resources (as a JV of SMIC) & won’t have a problem ramping up production. And if you question the ability of Chinese chip designers in developing competitive SiC products, may I ask you to take a look at the stuff Novosense has developed? Beyond that, what’s so special about SiC MOSFET that Chinese firms just can’t catch up in?

The number 1 SiC customer in the future is BYD and their goal is to produce everything in house. How can Infineon, ST & Wolfspeed all think they can capture 30% of market when BYD won’t buy anything from them? The answer is they cannot. Aside from that, Chinese automakers aren’t going to want Sic Modules that depend on American made wafers. That’s called unreliable supply chain. In the end, Infineon will also have to move production inside China if it wants to keep existing customers beyond 2025.. All their current Chinese EV customers also announced domestic SiC sources. Everyone is trying to compete on cost with BYD, which produces everything in house. How can you produce substrate in China, ship it to Malaysia, have it fabbed there and expect prices to be competitive with something fully designed and fabbed in China?

You cannot. ST will maintain good market share with its Sanan JV. Infineon and others can expect their share of the China market to be below 10% in a few years. Wolfspeed will get 0% of China market.