Why is BYD willing to start price war

We are 1 month into BYD’s price war on rest of the market. The full year 2023 report came out earlier this week and there were many questions about BYD’s margins for Q4 and projected margins for Q1. People keep asking why earnings dropped in Q4 vs Q3. Why is BYD a good investment if China has such a fierce price war?

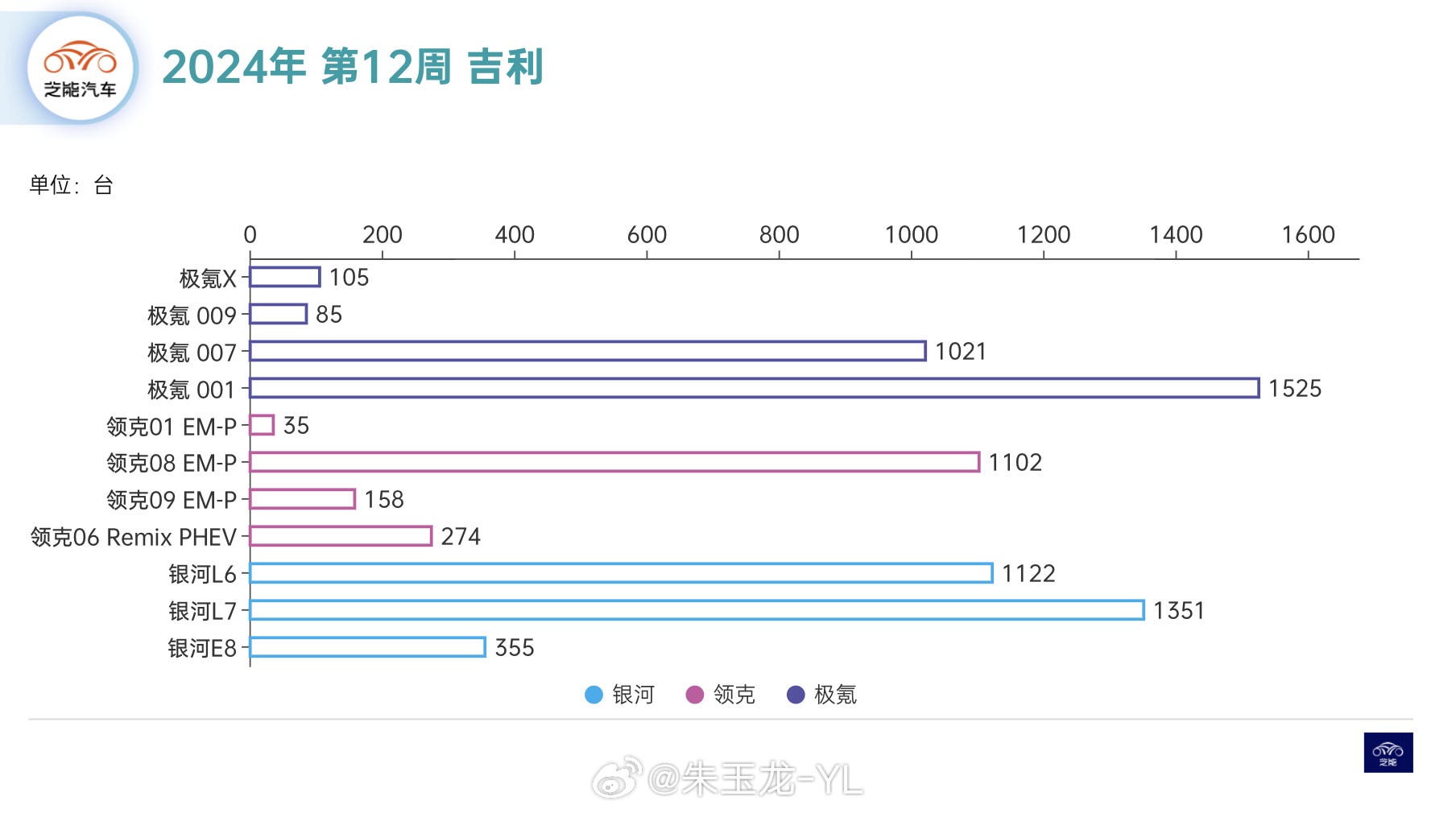

First, let’s explain why BYD’s Q4 auto division margins were down. As BYD started expanding its sales across the year, it suddenly hit a road block in September as Huawei Mate 60 launch propelled its entirely business. AITO M7 went from having no demand to having unlimited demand overnight after a refresh. At the same time, XPeng G6 & G9 came out and were priced quite competitively. It appeared that BYD really got caught off guard by this rapid movement toward smart car. BYD suddenly got the label of being bad at software. The much heralded Denza N7 completely tanked in sales after lower priced SUVs came out. N7 didn’t get Highway NOA update until January and has struggled for months. BYD’s NEV market share in China shrunk to about 30% for October and November as Li Auto and Huawei models caught fire. BYD was only able to hit its 3 million sales target through some aggressive discounting in December. That’s why it’s Q4 margins was weaker than Q3. Coming into this year, Geely launched several new models like Zeekr-007 and Galaxy E8 as well as refreshed Zeekr-001. Wuling launched XingGuang and Bingo Plus in a bid to capture market from BYD.

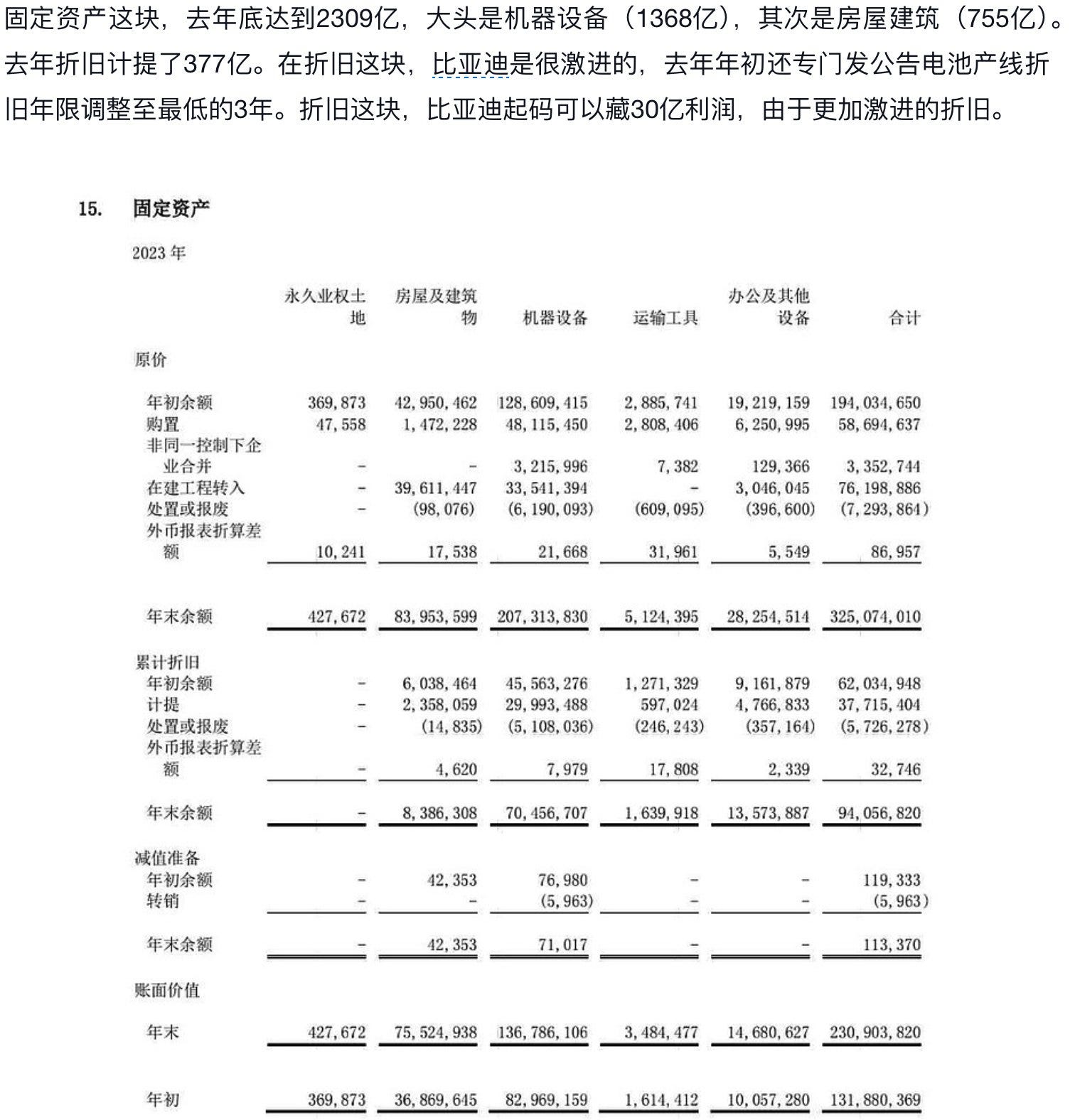

It was clear that BYD had to respond, because they had finished construction of several factory projects. Its fixed assets increased by 133B RMB from 2022 to 2023

It had a lot of capacity at this point and heavy depreciation coming over next few years. It had to sell more cars in order to spread out the cost of new factories and capital investments. It has 207B RMB of machineries by end of 2023. All these factories not only did assembly but produced all the parts of NEVs including batteries, chips, EPS, EPB, eMotor, eControl, sensors and more. Nothing showcased this more than its new $1.4B fab in Shaoxing that plans to produce 6 billion sets of opto microelectronics products per year. You don’t plant to produce that many LEDs unless you plan to install a lot of them in your cars.

Once we got to mid-February, news came out that BYD was going to launch a whole lineup of 2024 models that will be significantly cheaper than 2023 models. All this started with Qin Plus DM-i and Destroyer 05. Qin Plus 2023 models were selling for 89.5k RMB by December and did quite well. But by January, heavy discounting from legacy ICE sunk Qin Plus sales to 8th amongst compact sedans. In many ways, legacy ICE can afford to do this. Their factories in China are fully depreciated. The supply chains were fully depreciated. They weren’t making their cars better. They just kept discounting to attract sales.

At this point, the only thing BYD can do is break through ICE hold on price sensitive customers by its “electric is cheaper than gas” campaign. 79.8k RMB pricing on Qin plus and Destroyer 05 really moved the market. They have destroyed the compact ICE sales since their launch. April production for Qin plus and Destroyer 05 now expect to be over 100k. Similarly, launch of 2024 Seal DM-i, Han DM-i and upcoming launch of Qin L will likely put further pressure on well known sedans like Camry and Accord. BYD is really going after the entire legacy air supply chain and final production. Earlier this year, we have already seen massive layoffs from legacy supply chain. What will happen if the utilization for these ICE supply chain go down another 15%? That could happen if those Chinese ICE sales decline by 50% over the next 2 years. That is what BYD is going after. It wants to make ICE uncompetitive. BYD machineries have 3 year amortization period. They will be fully depreciated soon enough. Once NEV factories and supply chain are as depreciated as ICE ones, how does non vertically integrated ICE production remain competitive?

But it goes beyond just legacy ICE. BYD also does not want its domestic competitors from taking those market share with their own EVs. That’s why the price wars are also targeting Wuling, Geely and GAC Aion. It’s only NEV competitor sub 120k is Wuling. Now, it has Seagull, Dolphin, Yuan Up, Qin plus and Song pro all living in that segment. If BYD can make Wuling irrelevant, it would have complete control of that segment. For the segment about that, it had been facing pressure for Geely and GAC with multiple well priced models. But look at what has happened to Geely’s NEV registration numbers in recent weeks. E8 has sunk to below 400 per week. Zeekr 007 is back close to 1000. L6 and L7 are also a small fraction of Qin Plus and Song sales volumes. BYD wants to make sure Geely does not become a legitimate competitor.

If it can become the default in China’s automotive industry below 200k RMB, all its competitors are in deep trouble, because BYD has far and away the lowest cost.

The recent expansions will slow down, because it can only get so big. Its depreciation will come down. It’s R&D will pay off. 2023 was a major year of growth for BYD, but the past 6 months have been a struggle. Things are turning around again for BYD.