BYD semi growth

A few days ago, I heard something truly startling from BYD Exec Li Yunfei. At the China Auto Chongqing Industry summit 2024, Li said that BYD will start production at a new SiC fab in the second half of this year that will be the largest in the world and produce 10x what the second largest produces.

Previously, I talked about the future of SiC industry in China. I know about the increased scale of SiC substrate and epitaxy coming online from Chinese producers. I also know about the investment that BYD has made in SiC substrate and epitaxy production, but BYD is building a much larger SiC fab than those investment would suggest.

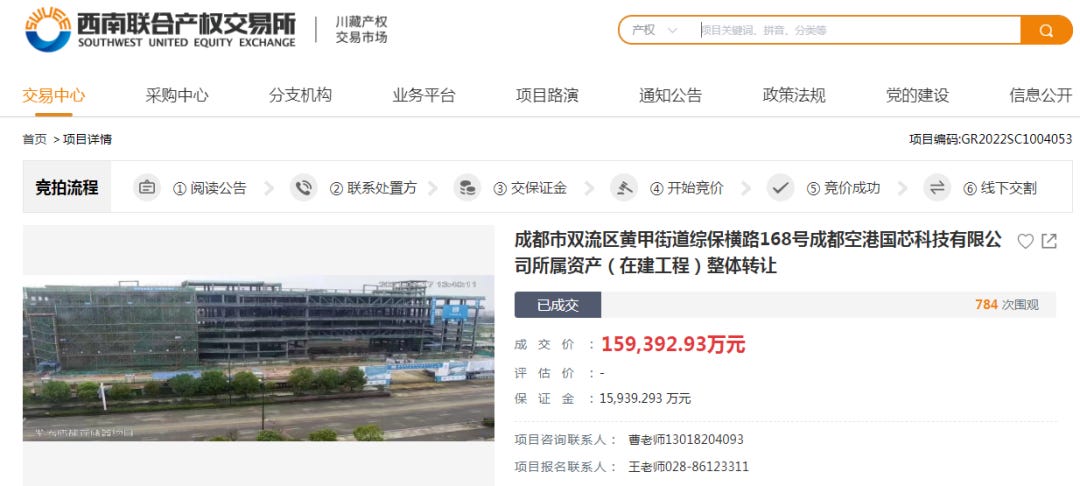

Back in December 2016, Unigroup invested 50B RMB for a new large memory chip fab at Chengdu, which would be its second large memory chip fab after its creation of YMTC in Wuhan. Work for this started in 2018, but halted in 2021 as Unigroup went through bankruptcy proceedings. By Aug 2022, BYD incorporated a new semi subsidiary in Chengdu and also took over the land that Unigroup was building on for a very reasonable sum of 1.59B RMB

That’s when we knew BYD was planning a huge fab here. The land is probably large enough for 300k wpm of memory chip production. Now, Unigroup also planned for adata research center, a smart city research center and industrial cloud research center and an industrial cloud base in its new Chengdu base. It remains to be seen if BYD plans a major R&D center here. At Nov of last year, we got news that Gree had won the contract to supply industrial AC units for this fab. This fab was clearly going to be larger than its existing fabs in Ningbo, Jinan and Changsha. I just didn’t know what they had plans. In the same month, we also heard that BYD was starting production at its Shaoxing fab. They planned to produce 720k Power IC modules & 6B optical microelectronics products per year here.

Just imagine how many EVs 6 billion LEDs can supply ever year. Everything BYD does seems to be aimed to supply a future where it is producing 10 million EVs a year. Back in 2022, BYD sales increased so quickly that its semiconductor plants could not support EVs with enough IGBTs even after Changsha and Jinan fabs came online. It had to buy chips from Silan Micro, SMEC and others. Even as it bought power chips from competitors, it had so much internal demand that its market share rose from 23 to 29% from 2022 to 2023. Even for SiC, BYD Semi market share had risen to 19% by first 2 months of this year (second place in China) on the back of usage by mostly its premium models. Since then, it has introduced the E3.0 Evo platform that promises 99.86% efficiency in its electric control through advanced SiC power modules

Since this platform will be used across a large chunk of its mass market models (rather than just premium four wheel drive versions of Han and Seal), I anticipated at the time that BYD demand for SiC was going to rise significantly. I just wasn’t sure whether it was planning to supply most of that internally or buy from SMEC or Sanan or others. More recently, it also introduced a 900V platform for its electric buses that extensively use SiC

While not explicitly stated, I think it’s also possible that DM 5.0 got this efficient through usage of SiC power modules or could be outfitted with SiC modules in the future. The demand for SiC on BYD vehicles is very high and BYD is meeting its challenge.

BYD’s efforts with SiC go far beyond just production. It has been involved with R&D efforts in SiC for a long time. You can see below just how its advanced SiC packaging has evolved from first generation HPD packaging used on Han to the recent third generation half bridge packaging in 2023

Beyond that, you can see from below that BYD’s chip products cover almost the entire car. The only notable exceptions are ADAS chip and cockpit chip. Not only does it design these chips, it also fabs most of its own chips.

BYD is also really good at ramping up production. Back in Aug of 2022, it signed deal to build a new fab in Yangzhoul to produce IGBT modules. By April of this year, BYD Yangzhou subsidiary already said it can produce power modules for 1 million cars this year, mostly IGBT module for DM 4.0. And it is quickly moving onto producing modules for DM 5.0. After Chengdu comes online, the next fab might be located in Wuxi, where many large fabs are located.

Beyond all of this, the most impressive part about their semiconductor effort is how early it started. They bought the semiconductor unit back in 2002, before they even had an auto unit. Back then, WCF already knew he wanted to build BYD into a huge EV and new energy supplier. In order to do that, he needed to control chip production to not have supply chain disruptions and keep cost down. BYD has focused on analog chips, power modules, MCUs and sensors chips that are critical to all its products. As of January of this year, Semi division has 5000 engineers! There are also additional engineers in ADAS division designing ADAS chips. BYD’s current semi talent pool is competitive with many of the leading semiconductor companies that make auto chips like Infineon, TI and ST. Of course, many of the hirings have come more recently. So, we won’t see the fruits of these hirings for a couple of years. However, it would be a mistake to doubt BYD’s ambitions here. Longer term, BYD Semi wants to self supply all of its cars as well as supply many other Chinese automakers. In fact, is already supplies Dongfeng, Renault, GAC, Chery, SAIC, Honda, Geely, ChangAn and GWM. This is a powerhouse that no one is really noticing, because it’s auto division takes all the attention away.

Great post as always! Thanks for sharing!

What's the best way for an individual in the west to invest in BYC? Any ETF ?