ICE to EV implication to automotive supply chain

The move from ICE cars to EVs have been a huge boon for China. Now, China is the #1 auto exporter in the world. But, how deep does this go? What is the implication on the global automotive supply chain?

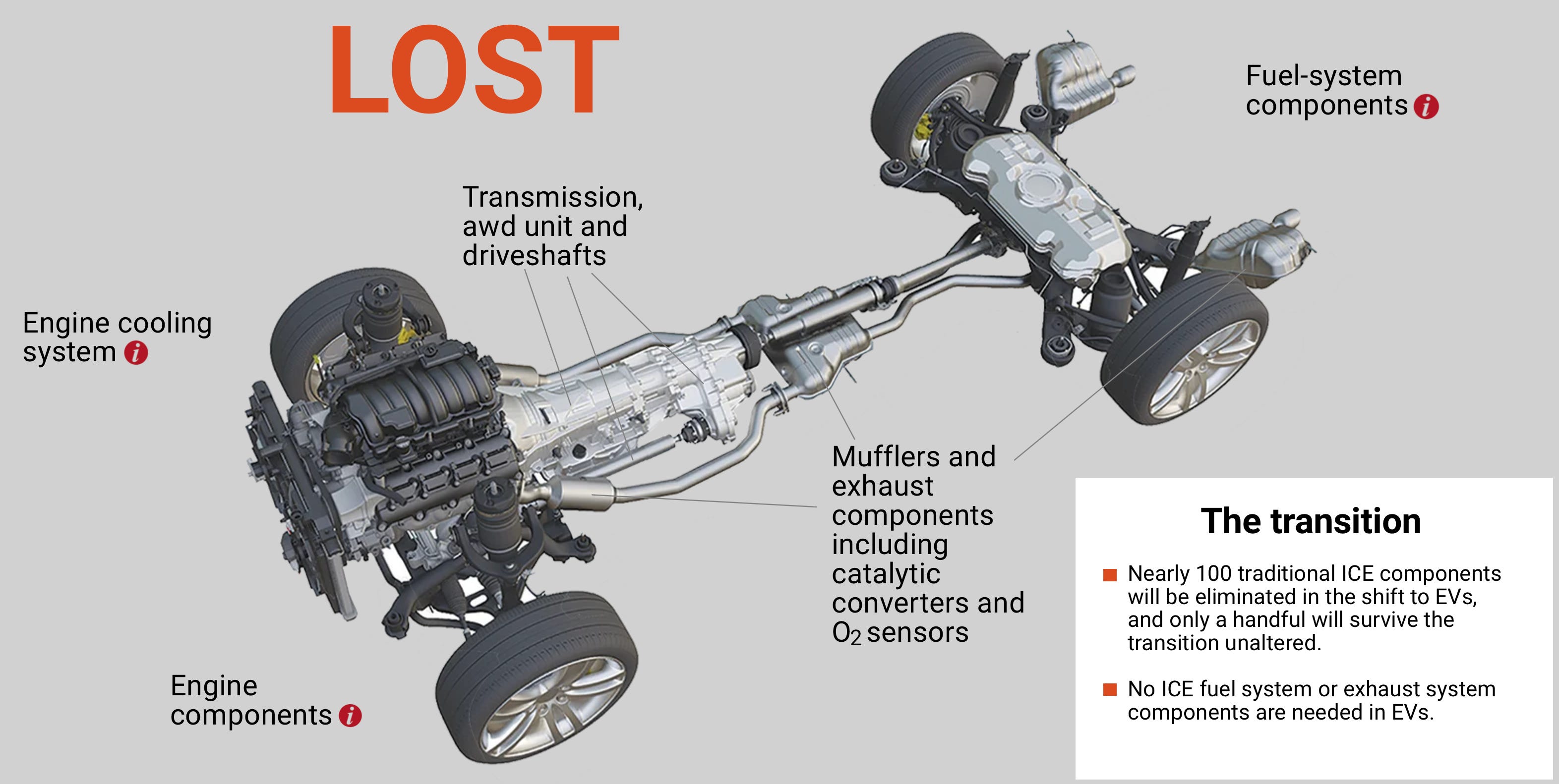

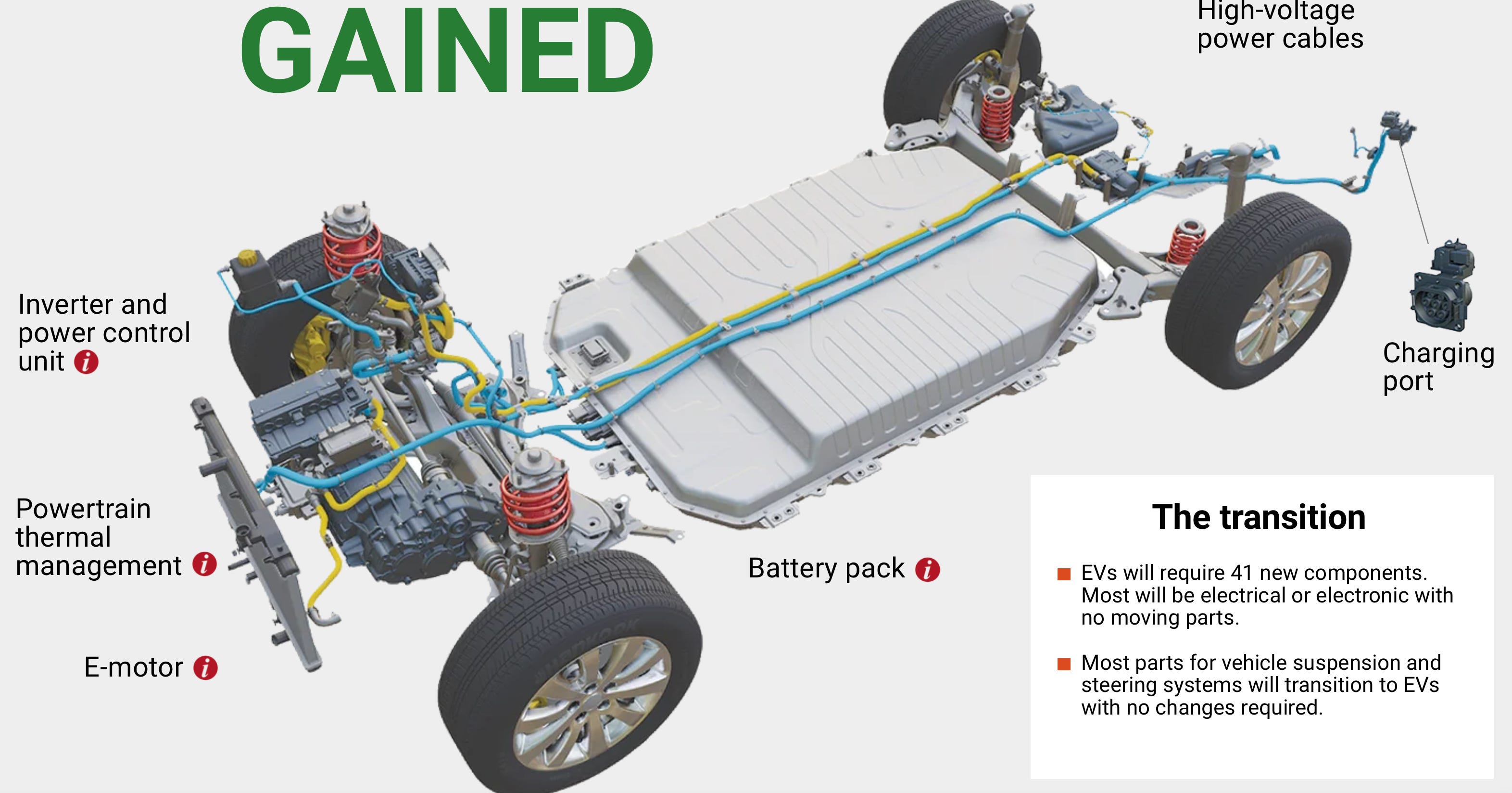

Recently, I tweeted about Electric Power Steering system showing just how dependent it is on different types of chips. In fact, as we saw with BYD’s recent U8 special concept car, even things steering column & braking calipers can be removed. It ran entirely on electrical system. ICE to EV is move from mechanical to EV

Engineers spent decades making internal combustion has efficient as possible only to be surpassed by electrical technology that’s simpler, more efficient & less costly to operate

The simplification resulted in dependence on chips, sensors & batteries as the cost drivers of EV/AV supply chain. This transition threw away all the legacy auto/supply chain R&D of past 100 yrs.

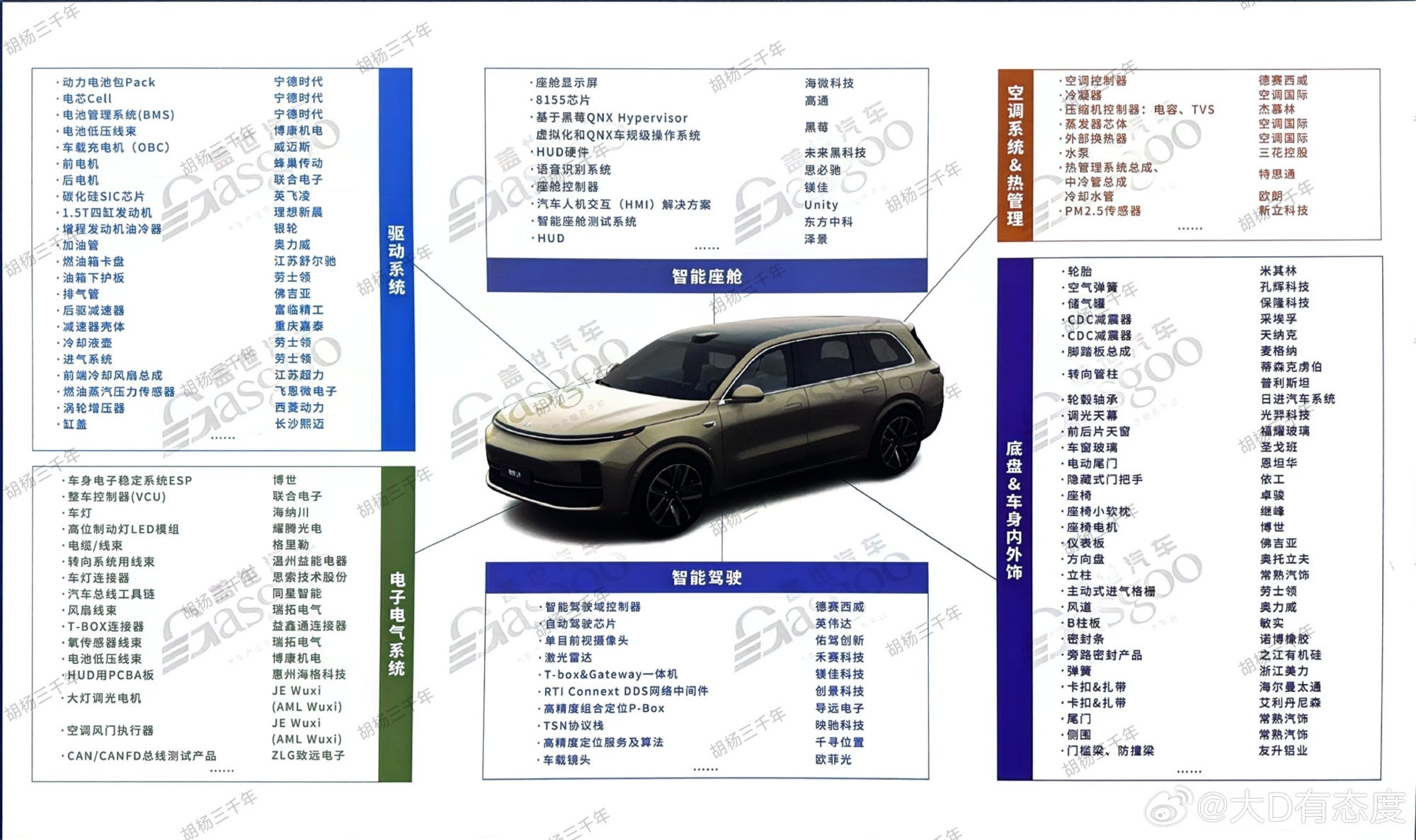

It’s been known for a while that Chinese companies dominate the battery supply chain, so I don’t need to talk about that here. I also covered the likely trajectory of Chinese Sic Market here. But what about other parts of EVs? A July diagram of Li Auto supply chain show that domestic supply chain do well with battery, eMotor/Drive & consumer electronics stuff whereas hi-end chips and more traditional related components like suspension system & electronic stability system are imported

Smart cars related stuff like ADAS & cockpit are almost entirely domestically supplied. Only foreign components are the core ADAS and cockpit chips from Infineon & QCOM. Germany/Japanese suppliers are shut out completely.

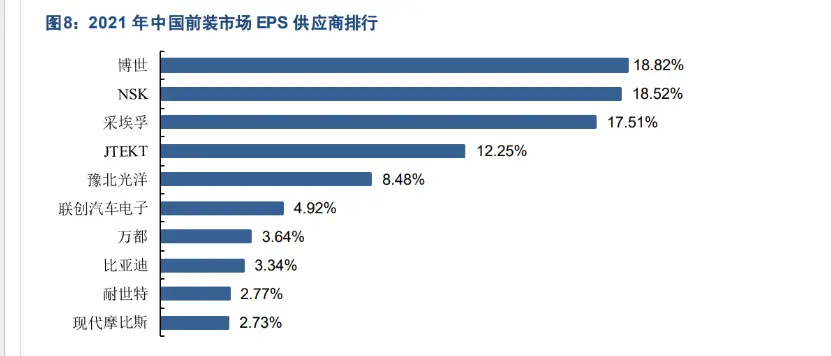

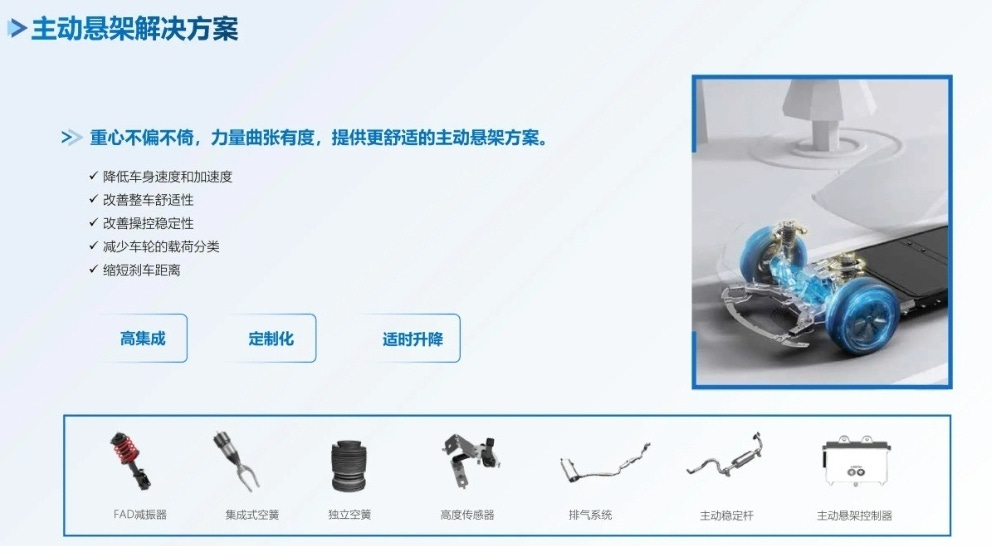

In important motor/driver/power/charging module related supply chain, the lists are almost always dominated by BYD/Fudi at top, followed by various domestic or JVs. And then there are things like EPS, EPB, air suspension & smart wheelbase. Here is a market share breakdown of EPS in 2021

Dominated by Bosch, ZF, NSK & JTEKT at top, but BYD/Fudi has been increasing over time. This is also happening in EPB & other electric system that’s driving mechanical control. As something like wheelbase & suspension system become smarter by automatically adjusting based on ADAS computation demand, these systems have become increasingly built domestically. Fudi offers a complete line of active suspension products

Due to the ongoing chip war, Chinese supply chain is actively looking to de-risk from Western chipmakers. That means, using domestic SoCs, MCUs, AI chips, power chips, PMICs, sensor chips, CAN chips, Serdes chips, eMMC, NOR/Nand Flash & other ICs. Recently, SemiDrive signed deal with MainRoad AI to use E3 MCU to control active suspension for various Chery Exeed models. This is the 1st domestic active suspension to use domestic MCU. This will also happen to all the BYD/Fudi & other domestic suppliers

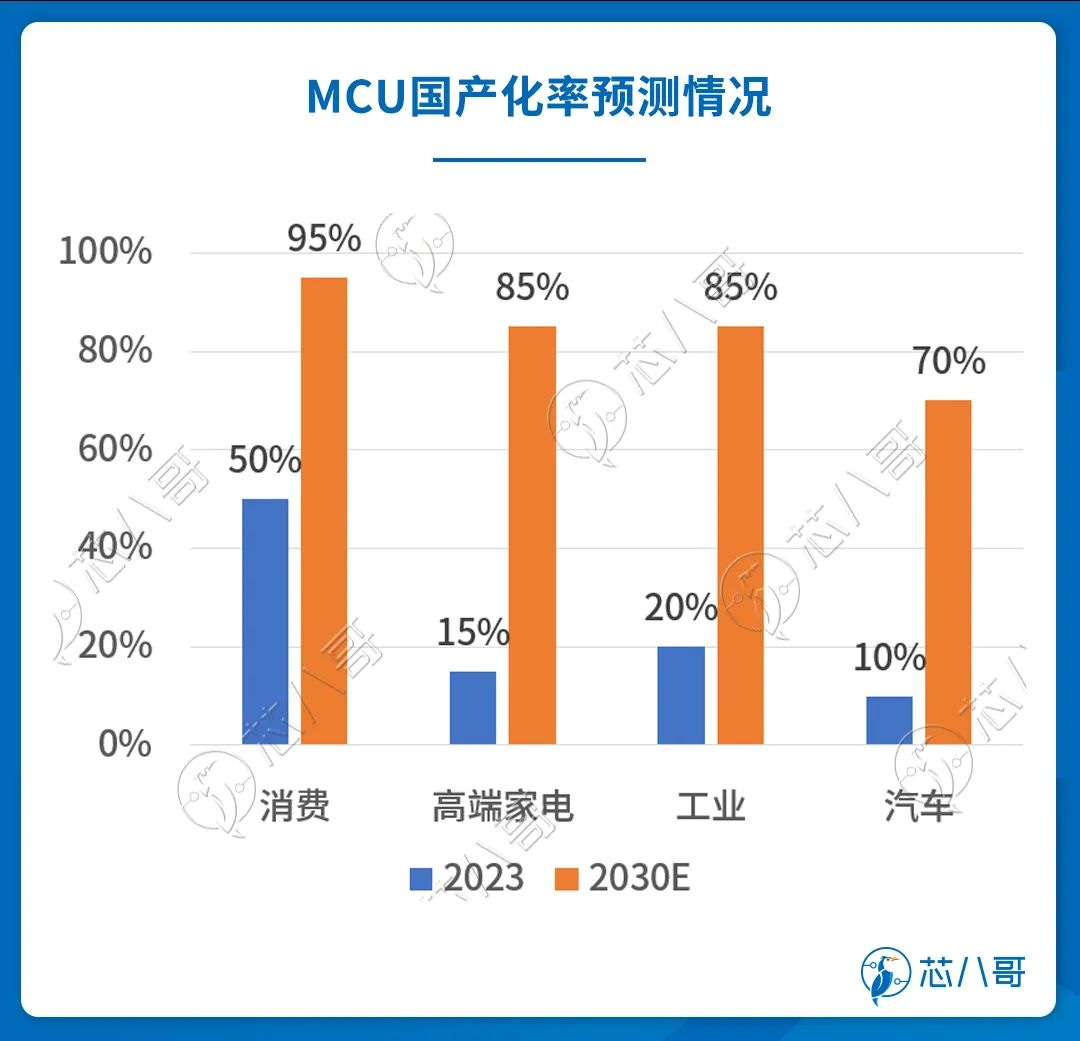

In fact, recently a domestic chip house estimate domestic market share for auto MCUs to rise from 10% this year to 70% by 2030.

Beyond that, there are increasingly capable domestic chipmakers producing whole suite of products that are auto grade and certified as TUV ASIL-B/D compliant. One example is Novosense, which anticipates it covers chip product worth 400 RMB per EV, but will increase to 2000 RMB before 2025

As you can see, it covers all type of control, sensor, PMIC, BMS, isolation products & other ICs. Many of these products probably aren’t technically super difficult, but cost enormous amount of money to get ASIL certification. That has been a major barrier for Chinese chip suppliers. But as firms like Novosense, Autochip, SemiDrive, Gigadevice & Norelsys gain more customers, they will also have the money to develop more auto grade products. That’s how this works:

Get funding & develop products & tape them out with fabs

validate products with domestic OEM

Achieve AEC-Q & TUV ASIL certification for product

Get large orders & use that to develop new product & certify them

One only needs to see the progress of Horizon Robotics to see a startup likely to become the top player in its field.

I do anticipate Chinese suppliers to not only achieve major market share in battery related stuff, but auto chips, eMotor/Drive/Control, wheelbase & ADAS products. I read a lot of fear mongering from American politicians about Chinese mature chip domination in the future. Well, just building fabs don’t shift market share. Market share only changes when customers want chips from these new fabs. The reason Chinese mature chipmakers might possibly achieve high market shre in the future is due to the huge market share of Chinese OEMs in EVs and major supply chain. This has led to rising market share of domestic chip designers getting contracts with OEMs & tier 1 suppliers. Which has led to demand for SMIC & other fabs to continue expanding their 28-90nm capacity.

That’s the big change from mechanical to electrical. Those who reached Industry 2.0 first dominated the mechanical engineering world. Industry 3.0 did not cause a fundamental shift in auto industry. But with AI & industry 4.0, we have finally moved from fossil fuel & mechanical engineering to EE. We are finally using drive/power/brake/control by wire. Those who are the best at EE, batteries & software/hardware integration are the winners of this transition.

Thanks for the deep dive!

Tiny nitpick - Infineon is German, was formerly the Siemens microelectronics business.

Can't emphasize enough, as mentioned in the article, that besides the tech, the big barrier to entry is executing automotive "quality system". Ie way of running a company that makes rigorous documentation *the* first-class organizing principle. And doing it at scale.

Perhaps for cultural reasons, Japan, Korea and Germany were particularly good at this around the turn of the century. US had mixed success, traditionally. Maybe now there is a mismatch where US still has some technological edge from leading edge chips, but the stronger manufacturing organizations are elsewhere? I think some EU subsystems manufacturers would be compelled by increasing cost pressures and shrinking market share, to merge with US partners. This is already starting, and ofc encouraged by US industrial policy. The results of such joint ventures have been mixed at best. Will be interesting.